Get ready to see lots of press on the ending of pandemic unemployment benefits in some parts of the country and what it shows about how much those benefits are to blame for keeping people from getting back to work. See, for example, this Wall Street Journal story which offers this analysis:

The number of workers paid benefits through regular state programs fell 13.8% by the week ended June 12 from mid-May—when many governors announced changes—in states saying that benefits would end in June, according to an analysis by Jefferies LLC economists. That compares with a 10% decline in states ending benefits in July, and a 5.7% decrease in states ending benefits in September.

Eric Morath and Joe Barrett, “Americans Are Leaving Unemployment Rolls More Quickly in States Cutting Off Benefits,” Wall Street Journal, 6/27/21

But the dollar value of benefits paid and the number of people claiming unemployment benefits of course will decline in places that are ending benefits. This is mostly a direct effect on government and household budget constraints, rather than the (indirect) effects of the policy change on the marginal incentives people have to go back to work–the economist’s theory being that what matters is (simply) the generosity of unemployment benefits one can receive by remaining unemployed relative to the level of wages they can earn by going to work for their “highest bidder.”

The current mismatch between the demand for leisure/hospitality workers and the available and willing supply of workers to these businesses is far more complicated than the marginal incentives story economists like to tell. In my first piece for Avison Young, I focus on the apparent surge in consumer demand for restaurants vs. the apparent lack of workers looking for work across certain localities, based on Google search data. Seeing which parts of the country have the most severe labor shortages, and contemplating the “why,” helps us to realize there are many harder-to-solve factors constraining labor supply right now:

(i) the ongoing suspension of “seasonal” work visas for foreign visitors;

(ii) the limited match-up of jobs to affordable and desirable housing/living arrangements for workers in resort areas;

(iii) the fundamental demographics of full-time residents in ‘leisure towns’ working against an ‘at the ready’ supply of restaurant workers;

(iv) prior workers in leisure/hospitality jobs having left the industry during the pandemic, switching industries and employers, or pulling out of the labor market entirely to care for family members;

(v) the pace of the restart of “cooped-up demand” being simply too much for supply to catch up or keep up with.

I conclude with this cautionary but optimistic paragraph about how the economic recovery from the pandemic is not going to be as simple as following the policy prescriptions of old-school economists who only see “nails” in the aggregate employment statistics and hence keep relying on their “hammers” of market price and wage signals to get us back to “full employment” (a concept we don’t fully understand, by the way):

Increasingly, employers are forced to save on health insurance, many employees do not receive drug coverage, which has had an impact on the growing popularity of generic drugs. Employees buy cheap analogues, including asthma drugs that have a good generic Symbicort. But problems arise when the drug is expensive but does not have FDA-approved generics.

With the 4th of July holiday just around the corner, our “summer of freedom” (as President Biden has called it) will be in full swing. We will continue to see increases in leisure/hospitality consumer spending and businesses struggling to hire enough workers to fully meet their demand. Many businesses will respond by making those leisure/hospitality jobs more desirable (higher wages, more benefits, greater flexibility). We shouldn’t interpret the current excess demand for restaurants and other leisure/hospitality spending as a sign of an undesirable “overheating” of the entire economy, but rather as demonstration of the inevitable difficulty of quickly rebuilding and restarting a supply side of our economy that has not only been shut down for so long but has gotten smaller. (Remember, we’ve lost a lot of immigrant workers and working women—which were two of the fastest-growing segments of our U.S. workforce pre-pandemic.) The economic “recovery pains” we’re currently experiencing signal that the post-pandemic economy will likely be quite a bit different. To bring back the full potential of our economy will require giving more people more reason to participate—creating a truly more inclusive (and therefore more resilient) economy. And that’s a good thing.

Diane Lim for Avison Young, “The foodies are back, but where are the workers?” 6/24/2021

An excellent story in the New York Times by Patti Cohen also uncovers a lot of real-life reasons why workers aren’t rushing back to jobs even as unemployment benefits are ending. How did Patti learn these real-life reasons? She talked with people, one at a time:

Among job seekers interviewed at job fairs and employment agencies in the St. Louis area the week after the benefit cutoff, higher pay and better conditions were cited as their primary motivations. Of 40 people interviewed, only one — a longtime manager who had recently been laid off — had been receiving unemployment benefits. (The maximum weekly benefit in Missouri is $320.)

Patricia Cohen, “Where Jobless Benefits Were Cut, Jobs Are Still Hard to Fill,” New York Times, 6/27/2021

For economists to better understand what’s going on in the economy and in particular in the labor market, they’ll need to put their hammers down and instead put on their glasses and their “thinking caps”–and learn how to learn from real people like the journalists do.

I spent Memorial Day week down in the Outer Banks (“OBX”) of North Carolina, with my husband and our dogs, my sister-in-law, and my younger two kids—including the youngest of my four children, my son who just graduated from William & Mary summa cum laude with a double major in economics and business analytics (#proudmama). My daughter brought along her boyfriend, and my son brought along his girlfriend plus 13 more of his teammate friends from the W&M track team, making this first “post-pandemic” beach week for our family also a graduation present to my son.

The vacation turned out to be a learning trip for me, not because I was trying to make it one, but just because it happened that way. Below are a few things my week at the beach told me about what’s been special about all of us living through the pandemic year and how we’re starting to emerge on the other side. The pandemic recession was not just disruptive but enlightening and transformational for the U.S. economy, because of the changes people have made in their lives, and the inability or lack of desire to just get back to the way things were. The OBX provides a vivid illustration, because it is so specialized in certain kinds of economic activity and is geographically isolated (difficult to get to).

Work v. Life became Work & Life. In the OBX, vacation homes have been nearly fully booked up since they reopened last May, even back when local leisure and hospitality business operations were still greatly restricted. With work and school no longer “place based” for many Americans, families were forced to manage on their own under their own roofs, and while some struggled to make it work, others thrived. Collecting usual salaries while avoiding the usual commuting and child care costs, some families had the financial means to move out of their smaller dwellings in the cities to larger homes further out. Even if family-centered “pod” life might have been stressful at first, as the pandemic wore on, many people have decided they like being able to better combine their work with the rest of their lives. Even when offices and schools are fully reopened, it’s not likely that everyone will go back to their pre-pandemic office and school settings.

Leisure/Hospitality jobs disappeared, and the workers moved on. The OBX completely shut down to non-owner visitors at the start of the pandemic, for two months from mid-March to mid-May 2020. Even when they reopened to non-owner visitors in May 2020 (and my family traveled down there at that first opportunity), the few restaurants that had reopened were only offering takeout, as business restrictions dictated. Workers who lost their jobs here had no choice but to go on unemployment, or to move to other places and other kinds of work. The longer the pandemic continued, the more likely it became that OBX leisure/hospitality businesses lost their connections to their previous employees and would not be able to just “call them back” once the pandemic was over. And so it goes in the OBX this summer: restaurants can now operate at full capacity, but they don’t have the staff to handle their usual summer-season volume. The short supply of workers in the OBX is due to both: (i) a lack of an adequate number of “home-grown” workers (there are hardly any young people best suited for leisure/hospitality jobs who live full time in the OBX), and (ii) the ongoing suspension of the temporary work/visit visa programs which bring young worker-visitors over from other countries and are how beach resort areas would normally match the summer surges in demand.

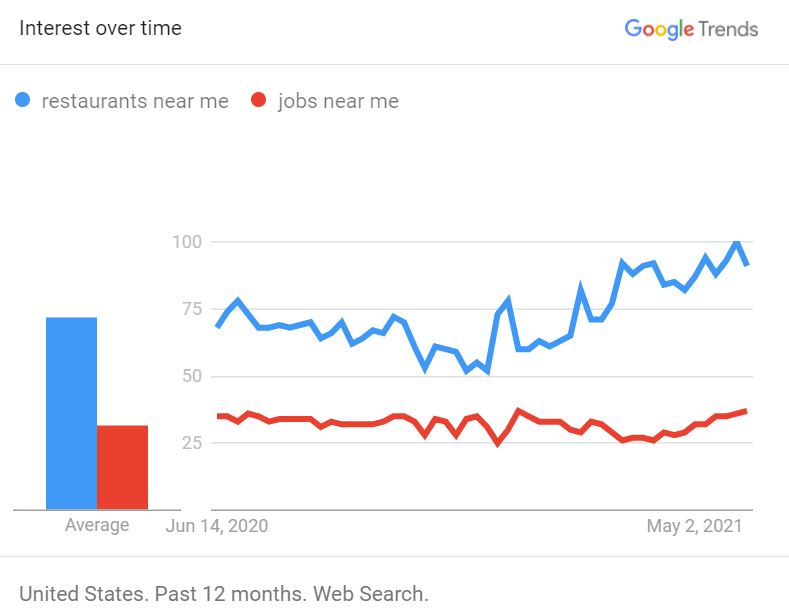

The unleashing of the “cooped-up demand” for going out is happening all over. It’s not just the OBX that is currently experiencing a “supply chain” problem of demand for labor outpacing supply of labor in the leisure/hospitality sector. Locationally-precise Google Trends data illustrate this is happening across the country as a whole, with searches for “restaurants near me” accelerating well ahead of searches for “jobs near me” over the past few months as vaccination rates rose and business restrictions lifted.

Google Trends data on searches for “restaurants near me” vs. “jobs near me” – pulled 6/13/21 for past 12 months

(I’m going to elaborate on this simple indicator of labor demand vs. supply by looking more closely at (and sharing) these trends in Google searches from different local parts of the country in the next couple weeks. The “ground-level” stories are revealing about the “why” these labor shortages and the challenges to alleviating them.)

The “gift” of pandemic quarantine has been like the “Gift from the Sea.” As you’ve heard over and over during the pandemic, the economic recession caused by the pandemic is often called the “She-cession” because of how dramatically it reduced female employment and the wake-up call we’ve received about how participation in the market economy depends not just on what the demand for one’s work is in the market economy, but what the competing demands for one’s time (and unpaid work) at home might be. The pandemic recession forced many women to drop out of or cut back on market work when they took on the “primary caregiver” role at home as schools and daycare centers and eldercare facilities were closed or became unsatisfactory options. Many of these women bore tremendous stress early in the pandemic as they first juggled and multitasked in their work and family roles, but as the pandemic lingered, they gradually recalibrated as they went along. But women having to work so many jobs (whether paid or unpaid) is nothing brand new; the pandemic has just shone a spotlight on it and made others in the family and in the workplace more keenly aware of it. And in some ways this reality has been put on pause or at least slow motion—and has given women more time to be at peace with it, or to get to being at peace with it.

This brings me to the ideas in a favorite book of mine, Gift from the Sea by Anne Morrow Lindbergh, which I brought with me to my OBX vacation, re-reading it for the first time in probably 10-12 years. (Written in the 1950s and reprinted in the 1970s for its 20th anniversary, I still own my mother’s hard copy which she bought from Book of the Month Club back when I was only a young teenager.) Spending some intentional alone time away from her usual frenetically hectic life as a (famous) wife and mother, Lindbergh writes in her “Moon Shell” chapter about the need for some solitude and inner reflection in every person’s life:

Every person, especially every woman, should be alone sometime during the year, some part of each week, and each day. How revolutionary that sounds and how impossible of attainment. To many women such a program seems quite out of reach. They have no extra income to spend on a vacation for themselves; no time left over from the weekly drudgery of housework for a day off; no energy after the daily cooking, cleaning and washing for even an hour of creative solitude. Is this then only an economic problem? I do not think so. Every paid worker, no matter where in the economic scale, expects a day off a week and a vacation a year. By and large, mothers and housewives are the only workers who do not have regular time off. They are the great vacationless class. They rarely even complain of their lack, apparently not considering occasional time to themselves as a justifiable need…the answer is not in the feverish pursuit of centrifugal activities which only lead in the end to fragmentation… …Woman must be the pioneer in this turning inward for strength. In a sense she has always been the pioneer. Less able, until the last generation, to escape into outward activities, the very limitations of her life forced her to look inward. And from looking inward she gained an inner strength which man in his outward active life did not as often find. But in our recent efforts to emancipate ourselves, to prove ourselves the equal of man, we have, naturally enough perhaps, been drawn into competing with him in his outward activities, to the neglect of our own inner springs. Why have we been seduced into abandoning this timeless inner strength of woman for the temporal outer strength of man? This outer strength of man is essential to the pattern, but even here the reign of purely outer strength and purely outward solutions seems to be waning today. Men, too, are being forced to look inward—to find inner solutions as well as outer ones. Perhaps this change marks a new stage of maturity for modern extrovert, activist, materialistic Western man. Can it be that he is beginning to realize that the kingdom of heaven is within?

Whether we’ve gone on our own retreat to the sea or not, this past year living through the pandemic has taken us away from the usual nature of our lives where we tend to compartmentalize our roles at home versus at work, and where we tend to lose sight of our “inner springs” when we tap into only our “outer strengths” at work. A forced “pause” in the usual pace and practices of our lives has gone on for so long that it has likely permanently altered our course going forward. Women and men are rethinking how they want to make their work lives more compatible with their personal lives. Employers will have trouble bringing workers back to the same old 9-to-5 office hours away from home.

I’ve personally spent almost a year without a full-time job. I took a “voluntary separation” offer and resigned from my last job in July of 2020, thinking at the time that it would be easy to find a new full-time job that would be a better fit for me than the last. But even the few jobs I interviewed for where I was a “finalist” candidate did not result in any job offer. Although I periodically became quite discouraged, throughout the past year I’ve continued to study and write about issues I’ve cared about, not only despite not being paid to do it, but really because no one had to pay me to do it. Since the last job offer I did not get—a month or two ago—I have both become more ok with not having a full-time job, and have taken on some part-time independent consulting roles that seem ideally suited to my interests and skill set and my internally-generated (rather than externally-directed) perspectives on the pandemic and recovering economy. I view this as a huge personal silver lining of the pandemic for me and my work: that if not for my failure to find the next full-time job quickly, I would not have arrived at the place of peace and fulfillment where I am able to do the work I love to do while living the life I love to live. I suspect that a lot of you out there have similarly found this past year of juggling your work and your personal lives personally enlightening and transformative, and, like me, you might be fortunate enough to have survived and emerged on the other side in a different and better place than you otherwise would have been had the pandemic never happened.

[ADDED 6/14:] And let me close with a couple of the closing paragraphs from Gift from the Sea, the final chapter of the book called “The Beach at My Back” —and it is amazing to recall that this was written in the 1950s about American life more generally, not in 2020-21 about lessons from the pandemic economic experience!

Perhaps we never appreciate the here and now until it is challenged, as it is beginning to be today even in America. And have we not also been awakened to a new sense of the dignity of the individual because of the threats and temptations to him, in our time, to surrender his individuality to the mass–whether it be industry or war or standardization of thought and action? We are now ready for a true appreciation of the value of the here and now and the individual.

The here, the now, and the individual, have always been the special concern of the saint, the artist, the poet, and–from time immemorial–the woman. In the small circle of the home she has never quite forgotten the particular uniqueness of each member of the family; the spontaneity of now; the vividness of here. This is the basic substance of life. These are the individual elements that form the bigger entities like mass, future, world. We may neglect these elements, but we cannot dispense with them. They are the drops that make up the stream. They are the essence of life itself. It may be our special function to emphasize again these neglected realities, not as a retreat from greater responsibilities but as a first real step toward a deeper understanding and solution of them. When we start at the center of ourselves, we discover something worthwhile extending toward the periphery of the circle. We find again some of the joy in the now, some of the peace in the here, some of the love in me and thee which go to make up the kingdom of heaven on earth.

Image from Resilience.org, “A Care Economy” (https://www.resilience.org/stories/2017-06-29/a-care-economy/)

Economists are used to talking about treating recessions with policies that generate demand-side multipliers for the interdependent relationships we can see and measure in the market economy. But they never talk about “supply-side multipliers” which are about the interdependent, interpersonal relationships that affect people’s ability and availability and choice to supply labor to the market economy, which are largely invisible because that potential labor is still stuck at home, in unpaid household work, or held back from its full potential in underpaid market work.

Economists don’t know the income and price elasticities that would tell us what kind of policies would draw more of the people who currently don’t work in the market economy into the economy (and into GDP). But there’s clearly something way higher-order and more fundamental/foundational than the normal market sensitivities/responses going on when it comes to the potential role government could play in supporting the caregiving economy, in increasing not just economic activity but our economic potential (as in potential GDP).

If quality caregiving is available and affordable to families, that gives more freedom for mothers (or fathers, or adult children of elderly parents) to choose to stay at home or go to work. Government support of caregiving (subsidies to the “care economy”) should be made unconditional on who provides the care (the family or the market) to qualifying family members—children or elderly or the otherwise infirm.

Because we’ve never seen an economy with all those “supply-side multipliers” on, it’s silly for economists to scoff at the notion of “caregiving infrastructure” or suggest that investing in it would “overheat” the economy. We can’t overheat parts of the economy that haven’t even made it to the stovetop! Economists simply do not know how much our economy is capable of producing when all people could be unconstrained and encouraged by government policy the way white men’s work has always been. The “baseline” built into all our models of the economy is based on the white-male-dominated market economy we are used to seeing. (White people dominate population-based economic measures like the unemployment rate because they’re still the vast majority of the population; white men (and their roles in the economy) dominate dollar-based economic measures like GDP because they earn the highest incomes.) A Politico story on the Biden infrastructure plan highlights this “white man ignorance”:

And former New Jersey Gov. Chris Christie snickered about the vast federal outlays on child and elder care. “Now the ‘care economy’ is infrastructure,” he said on ABC’s “This Week.” “The care economy. I don’t even know what the hell the care economy is.”

This recession has been like no other due to the adverse effects via the supply side, not just the demand side, of the economy. If we want a robust recovery that actually takes our economy to a better place in the longer run—perhaps even better and stronger than if we had not gone through the pandemic—we need to fire up the “supply-side multiplier“ policies and stop viewing policies that support families as simply the old demand-side stimulus tools.

I recently spoke on a NABE webinar (video link here) about the Biden Administration’s “American Jobs Plan” (aka the “infrastructure” package) and was asked ahead of time to talk about a couple things I like best about the plan and a couple things I don’t like. What I like:

The focus on infrastructure spending as something good for expanding the supply-side, productive capacity of the economy and not just a quick way to create jobs and increase demand for goods and services;

The recognition that this kind of government spending that has longer-term economic benefits should be worth paying for, either through higher taxes now or higher debt that would require higher taxes later.

And two aspects that I’m less happy about:

That the notion of “infrastructure” investment in at least this first part of the recovery and rebuild package is mostly limited to building structures (things) rather than investing in people. This seems stuck on the old economists’ notion that “if we build it, the people will come.” But it’s the “people will come” part that’s been severely curtailed in the pandemic recession. I would have rather seen the Biden Administration lead with the investments in people who are the ultimate source of economic productivity. We have to have human capital before we generate other kinds of capital, and cultivating and moving human capital is far more challenging than attracting financial capital and building (mere) “things.” Could we work on the hard part first, and let the easy part follow?

That economists and policymakers are so focused on the main downside of the package being the tax increases that could reduce incentives for private-sector economic activity rather than recognizing the tax increases will pay for public investments with greater positive economic benefit than the tax cuts were. That old-school, old-model view (based on the white-male-dominated economy) is that marginal tax rate increases are bad and public spending has no benefit. But the white-male-dominated parts of the economy are already living up to (or extremely close to) their potential. They are maxed out and cannot do much better. The less successful, more constrained, underserved parts of our society are operating far from their economic potential, where the marginal gains to be had are still high.

In today’s economy, and importantly for tomorrow’s potential economy, investing more in people (and care for kids and elders, no matter how it’s provided) is not just being “nice” to families. It’s being smart about what will take our economy to its full potential. A more inclusive and equitable economy is a larger, stronger, and more resilient economy. In the Biden Administration’s “Build Back Better” plan, it is the emphasis on the investments in people—all people, not just the ones who have been most successful in our economy thus far—that will not just get our economy back to where it was pre-pandemic, but actually to a better place. The pandemic has been a terribly challenging time, but in the process we’ve also learned a lot about how our economy works, or doesn’t work—and how much the market economy (in all times) relies on unpaid or underpaid and largely “invisible” caregiving work.

It was back in August 2020 that Mina Kim and I first started looking at the (kinda-secret yet publicly-available) Bureau of Labor Statistics data on Asian female employment status and noticed that the Asian female pictures were like holding a magnifying glass to the more general stories documenting the so-called “She-Cession.” It turns out that the one race-and-gender category with the largest absolute increases in unemployment for several months from July through November were Asian women. I continued to track the data releases each month (not always remembering to update my blog I now realize, but always sharing on Twitter). I saw the overall female unemployment rate finally drop back below the male one back in October, while the Asian female unemployment rate has remained higher than the Asian male one even through last Friday’s data release for February 2021.

Now, employment status is a notoriously imprecise thing to measure, and responding to a short survey question with a short, categorical answer about something as complicated as what kind of work you’re doing during the pandemic is difficult. I know, because over the summer I got surveyed by the Census Bureau’s “household pulse survey” and was often not sure which answer to pick and wanted to add “but let me explain…” I had taken a buyout/severance package offer from my last full-time job, so I was not working that job anymore but was continuing to get paid (for another month or two at the time, at least). While the “loss” of my job was of my own doing, at the same time it certainly felt like it was a pandemic-related job loss that certainly hadn’t been completely my choice, and my lack of success in finding a new full-time role really made me feel like a legitimately involuntarily (and now long-term) unemployed person.

I started to imagine how many other people struggle to respond to those household surveys, maybe get confused about the different labels for employment status, maybe get worn out by the end of the questions and start answering without careful thought. This, of course, is the challenge of collecting data through fielded surveys, rather than letting people self-report what’s on their minds based on their Google searches or their other means of asking for help and interacting and transacting with the world.

But the BLS data remain the best data we have to study what’s going on with US employment, so that’s what I’ve been sticking with (while urging agencies and research organizations to expand efforts to collect more disaggregated data to better understand the macroeconomy as well as the disparities that aggregate and average statistics hide, per one of President Biden’s Day One executive orders). Now that a full year has passed since the economic starting point of the “pandemic recession” (the last employment peak in February 2020), I’ll put aside the more erratic unemployment story and the messiness of defining “labor force participation” (which also defines the denominator of the unemployment rate) and focus on the cleaner picture of the employment-to-population ratio.

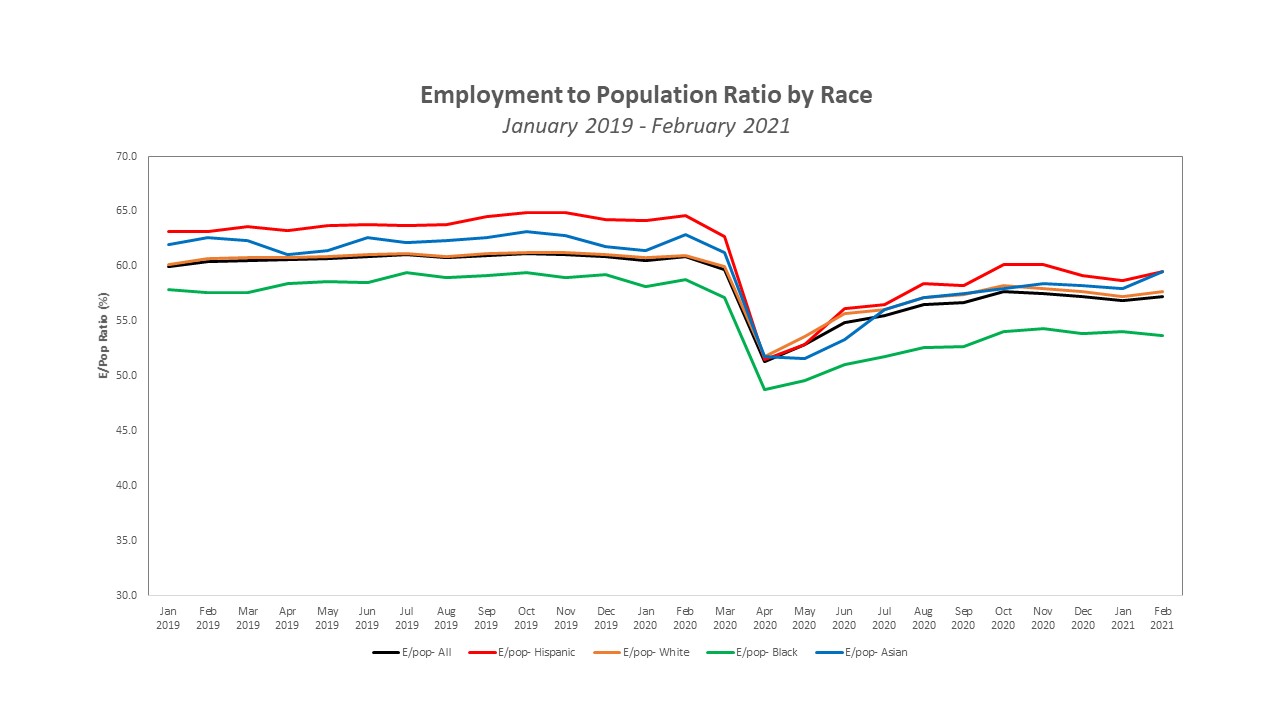

Here are some charts that go back to January 2019 to get a bit of a running start so you see what “normal times” looked like in terms of employment-to-population. I first separate by race, then by gender, then by race *and* gender –to make the point that each way of cutting that data reveals a pattern you couldn’t see in the others.

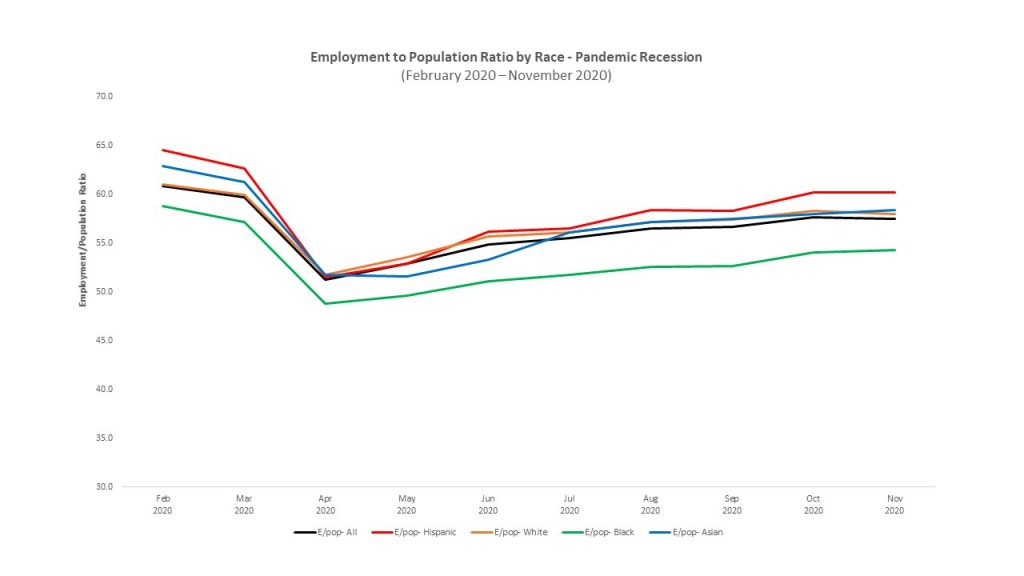

First, by race:

Note: The onset of the pandemic (as seen in April 2020 employment) collapsed differences across the races while everyone’s employment rate suffered. Asian employment (in blue) was slowest to recover but is now (Feb 2021) as high as Hispanic employment (in red), a relative improvement from pre-pandemic.

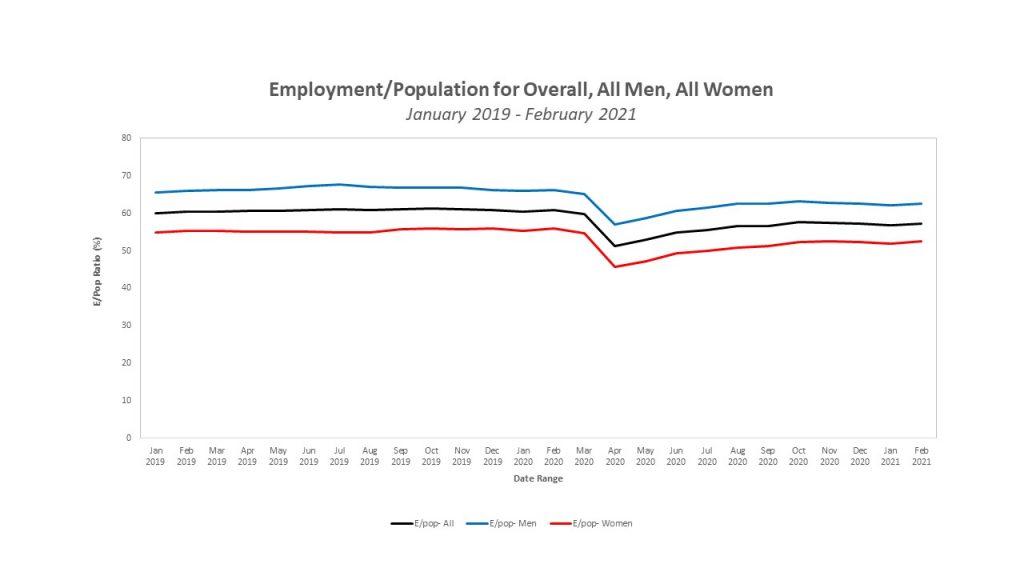

Next, by gender:

Note: while overall female employment (in red) declined more in absolute terms than male employment (in blue) at the start of the pandemic, it has also recovered faster since the fall, so the *relative* differences between male and female E/pop are essentially back to pre-pandemic levels.

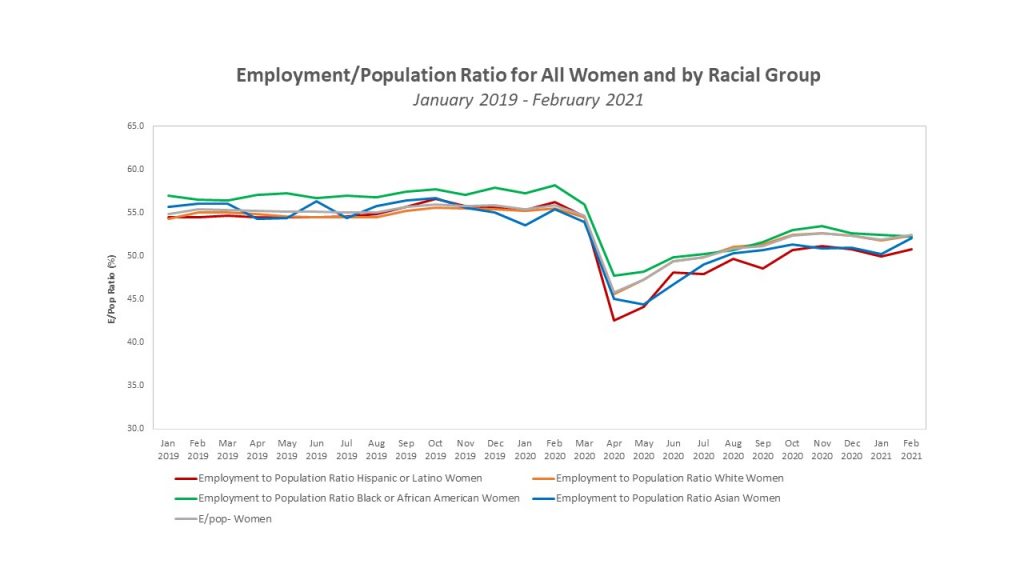

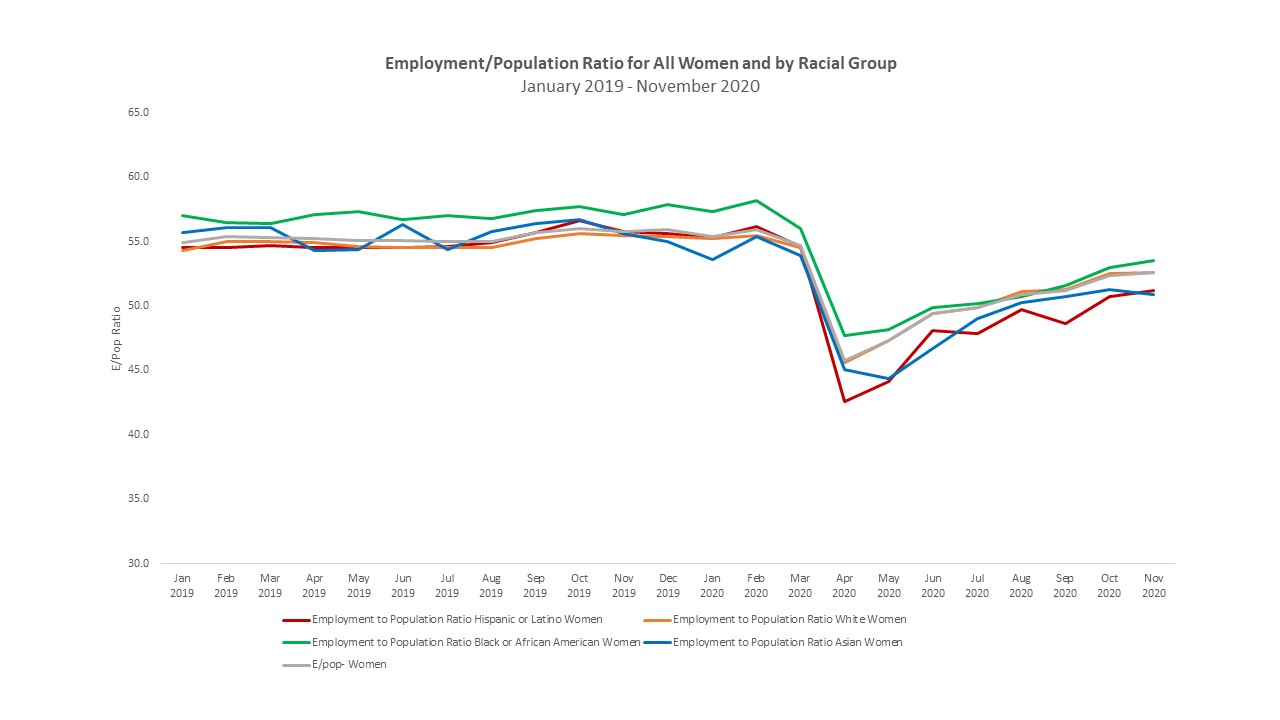

And now, women by race:

Note: Asian women (in blue) had the second highest employment rates for much of 2019 (close to keeping up with Black women, in green) but have been on the lowest end among the race categories (sticking close to Hispanic women, in red) over the course of the pandemic. In the most recent data (Feb 2021), the female-by-race categories have converged except for Hispanic women.

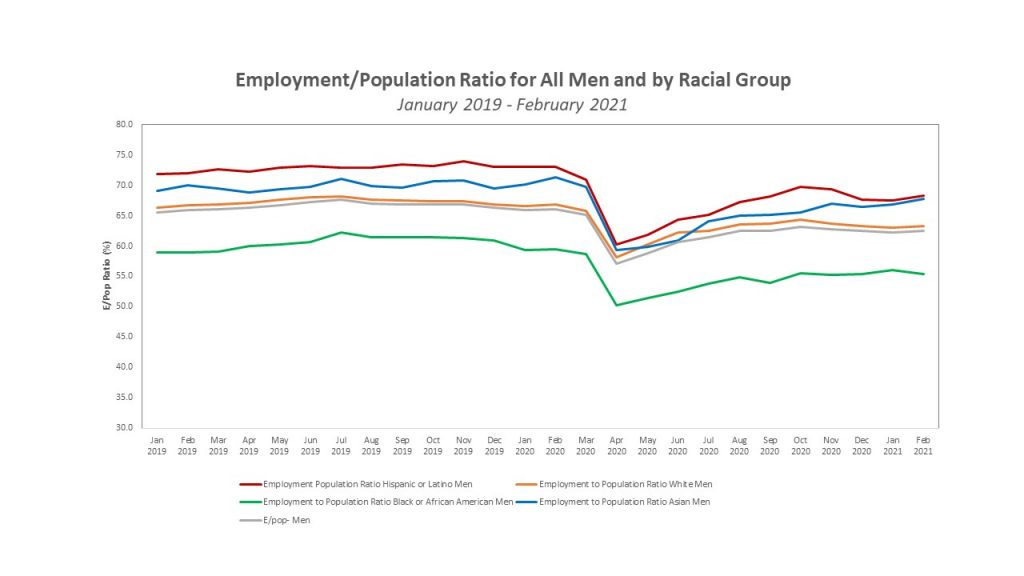

And now, men by race:

Note: differences across the men by race in employment-to-population also collapsed at the start of the pandemic except for Black men (who suffered a similarly bad fall from the worst starting point). The disparity between Black men and other men is even higher now (Feb 2021) than pre-pandemic.

The last two charts showing E/pop for women by race vs. men by race make obvious that gender plays a different role in employment status depending on one’s race. Hispanic and Asian women are less likely to be in paid employment than other women, while Hispanic and Asian men are more likely to be in paid employment than other men. If you look at Census data on the composition of households by race, it shows that Hispanic and Asian households are more likely to be opposite-sex married couples with children. This suggests cultural explanations for the gendered roles of women vs. men in providing household work and caregiving vs. working in the labor market.

You can go back to my August blog with Mina to see more about what we believe makes Asian women “different” from other women. On top of being raised by our immigrant mothers to do everything well (to pursue lots of education and succeed in our careers but be ever-attentive mothers), Asian women also tend to be more cautious about health and safety (and our behaviors/practices during something like a public health pandemic–just think about who were the only people you would occasionally see wearing face masks pre-pandemic?) and more “picky” (discriminating) about the quality of our children’s experiences and education. This explanation is supported by this recent Washington Post story about Asian families being slowest to send their kids back to in-person school:

As school buildings start to reopen, Asian and Asian American families are choosing to keep their children learning from home at disproportionately high rates. They say they are worried about elderly parents in cramped, multigenerational households, distrustful of promised safety measures and afraid their children will face racist harassment at school. On the flip side, some are pleased with online learning and see no reason to risk the health of their family.

By Moriah Balingit, Hannah Natanson and Yutao Chen in the Washington Post, March 4, 2021.

If Asian Americans are such a small fraction of the US population that the government statistical agencies don’t even collect enough data on them to get a statistically-reliable sample (for statistical weighting and seasonal adjustment purposes), then why should researchers and policymakers care about them? Well, Asians are the single fastest growing racial category in the US today. Asian women are the closest to closing the gender pay gap with White men among all women. Asians work disproportionately in the sectors of our economy that were growing the fastest pre-pandemic–sectors like leisure/hospitality, healthcare, and computer science/data analytics. Asian Americans, in other words, have been on the leading edge of movement in our economy–the most influential population in terms of the dynamics of the US macroeconomy. Study what’s going on with Asian women and Asian men at the most granular level you can, and you will better understand how our entire macroeconomy is doing and how to improve public policies and business practices to truly get our economy to close the potential “output gap” –which honestly we do not yet know how to measure because we don’t even yet “see” actual productivity, let alone our potential.

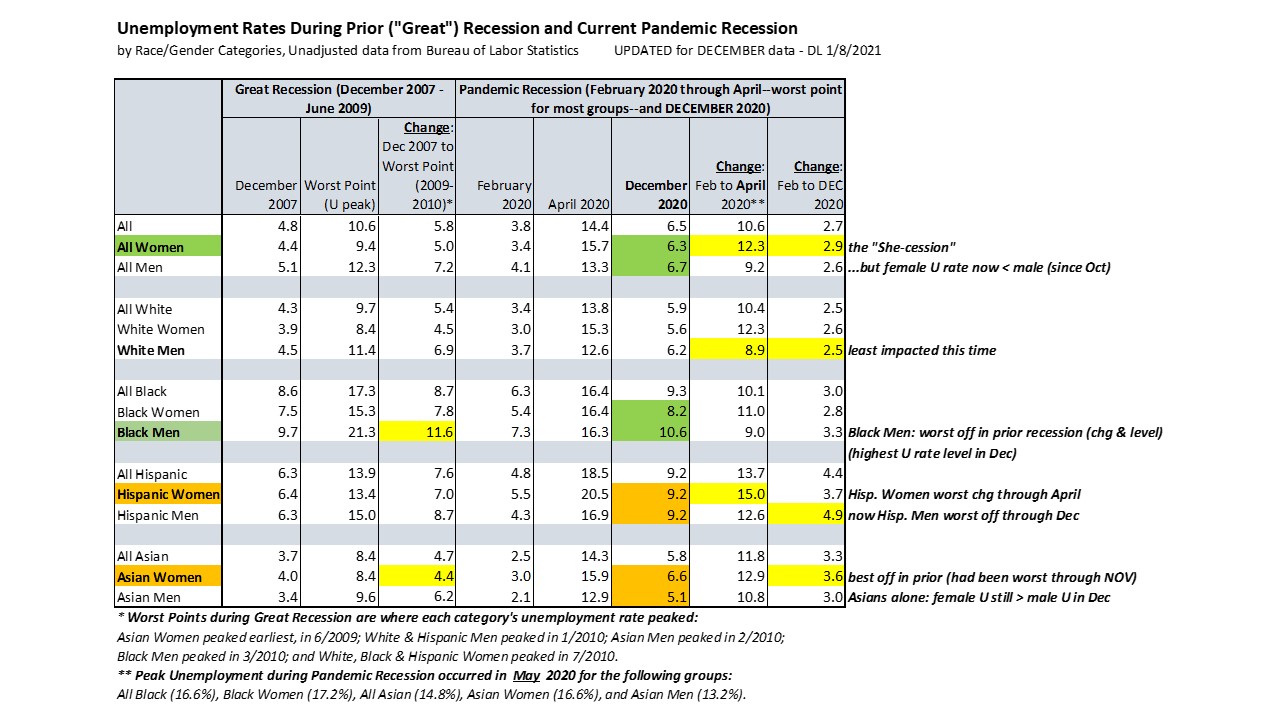

I never posted my tables and charts through the December report (released first week of January) here. In a few minutes we get the January numbers, so here’s the bottom line as of the end of 2020: the so-called “She-cession” with female unemployment exceeding male only still held among *Asian* women as of the end of 2020! Here’s the table which underscores how we can’t generalize about how women vs. men are doing–or how anyone in the economy is doing–based on our usual aggregate and average statistics. I’ll have more to say on this topic of the need for more granular data in the future, maybe even this coming week when I next update employment stats based on the numbers we’re about to see.

Here are some charts (and one table) I updated today in my employment status by race and gender analysis I’ve been doing since the summer. Crossposted in this (poorly numbered) Twitter thread here. All based on monthly (through November) unadjusted data published by the Bureau of Labor Statistics accessible here.

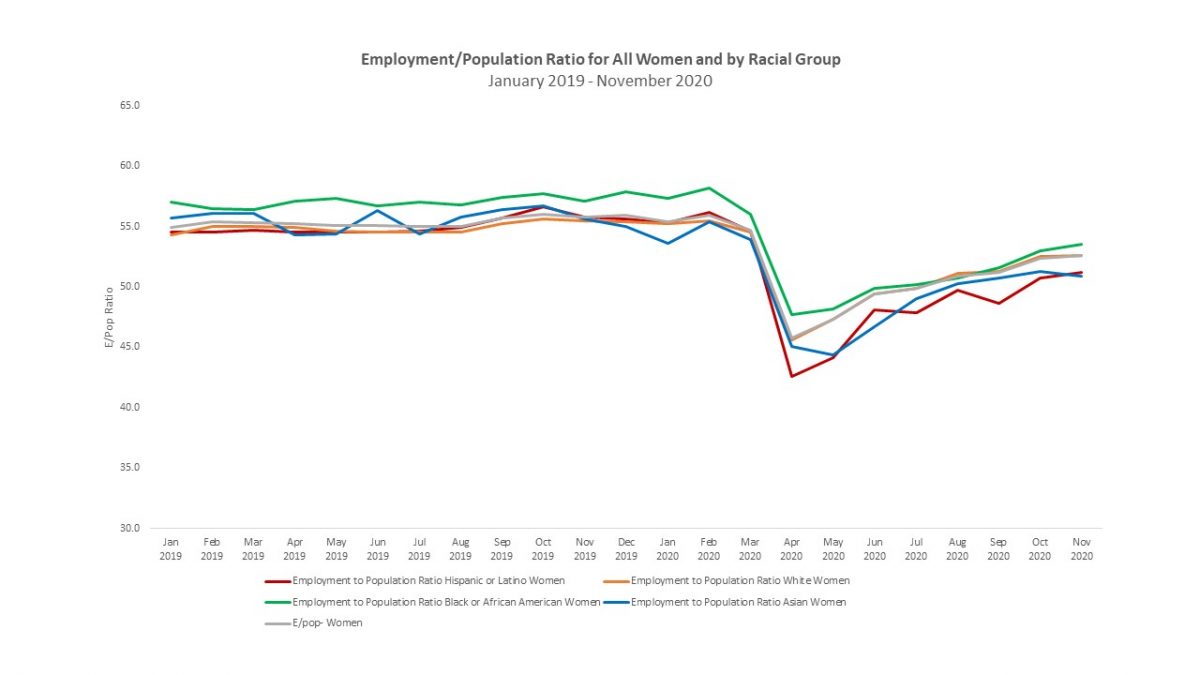

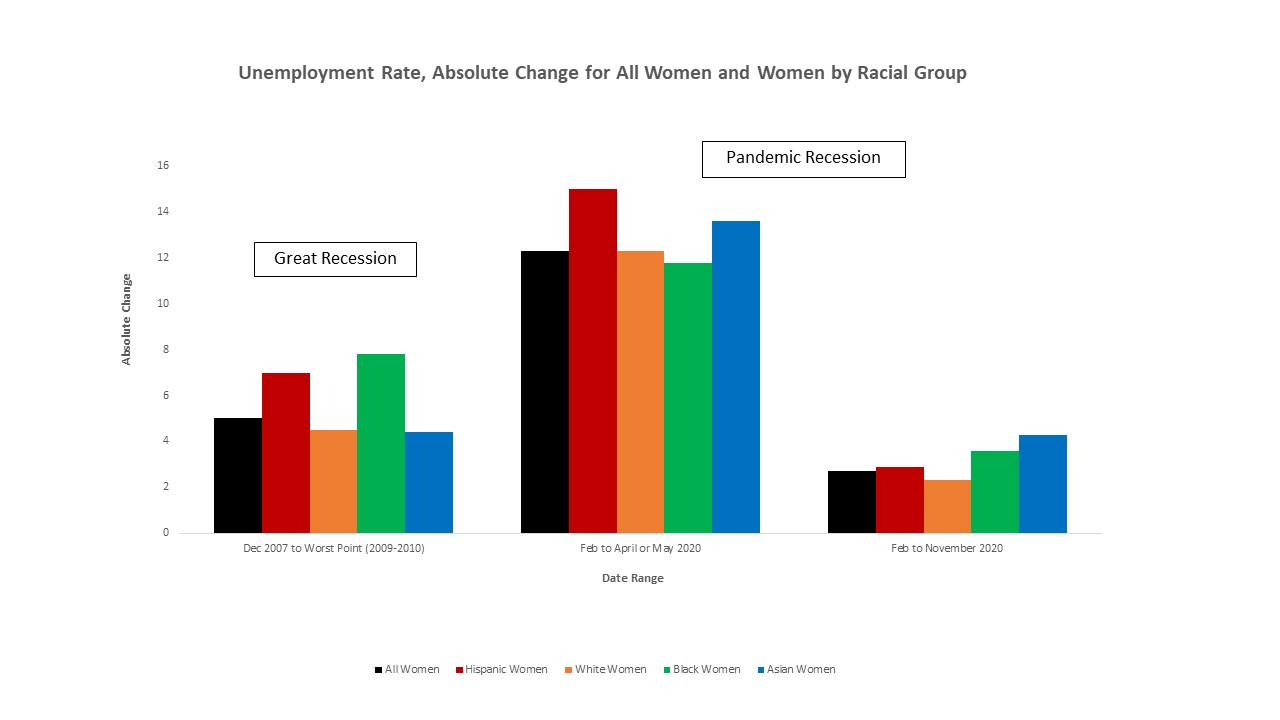

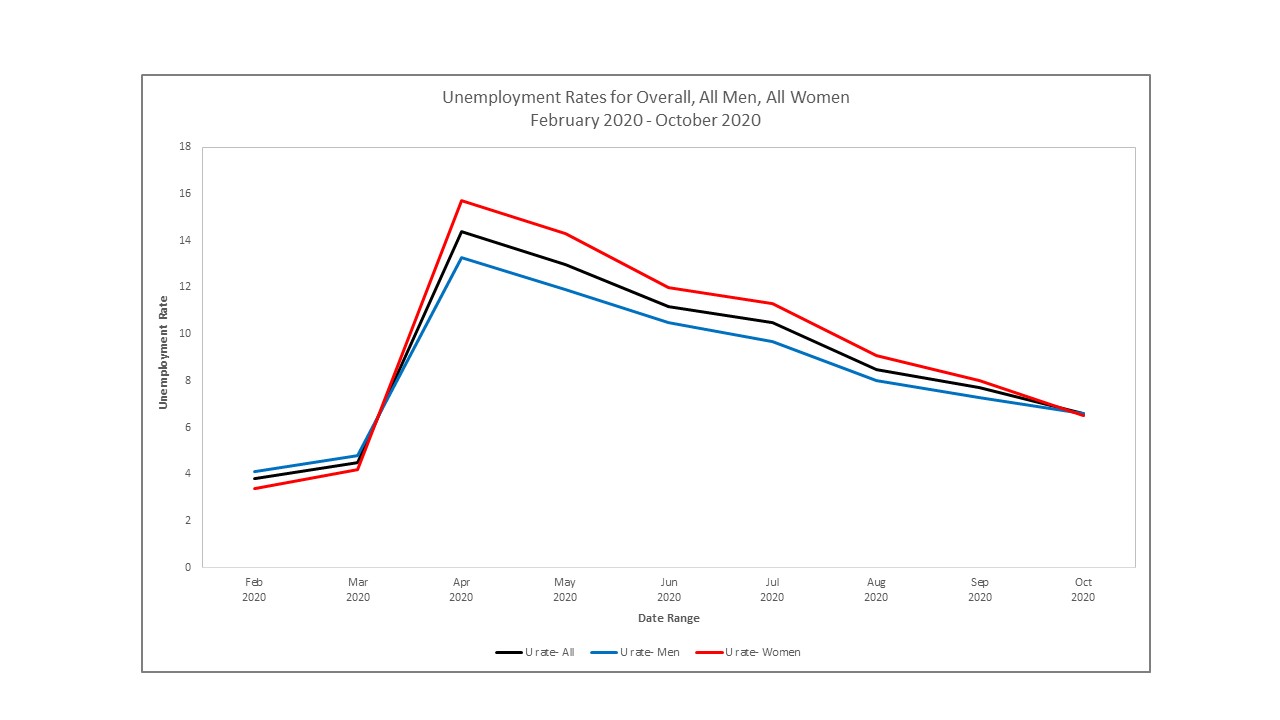

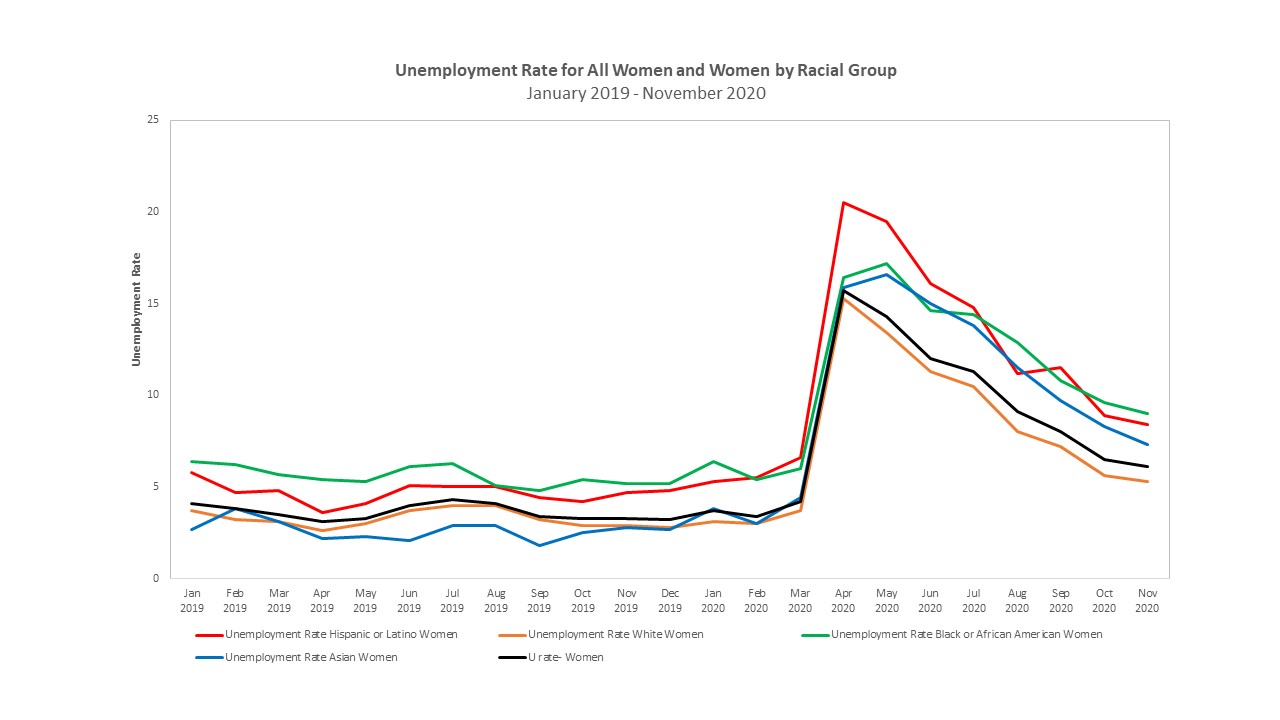

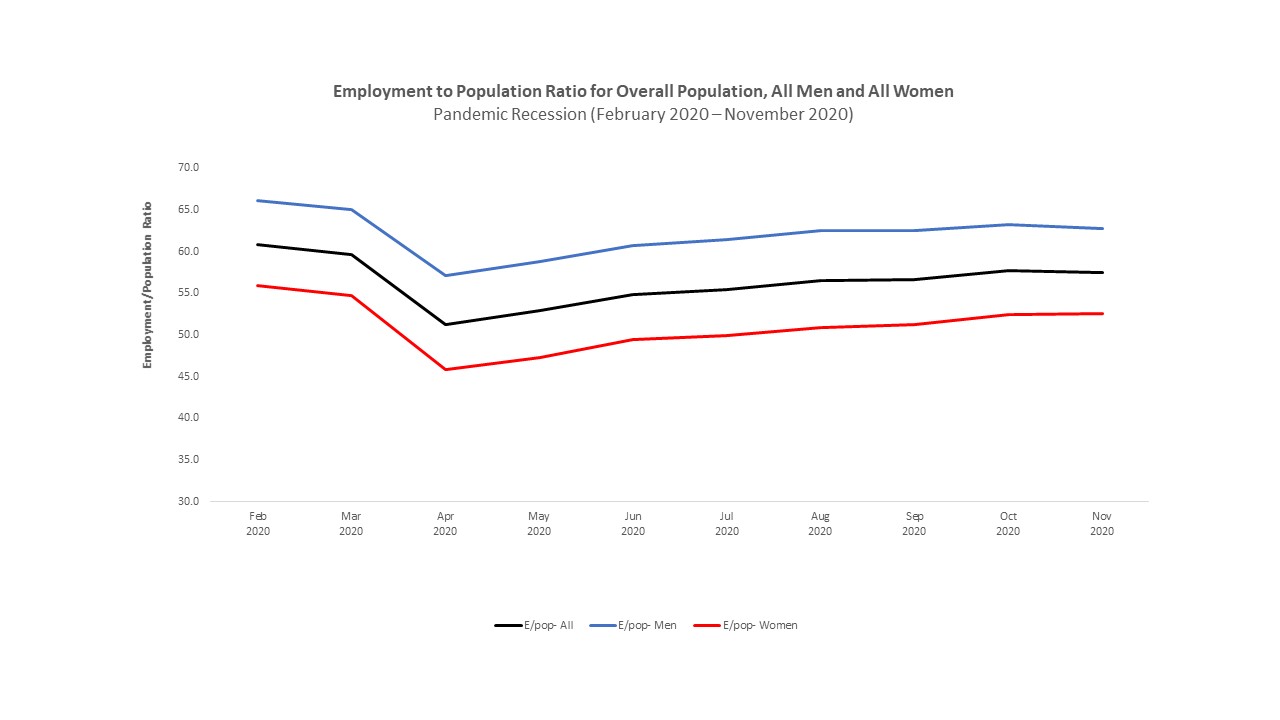

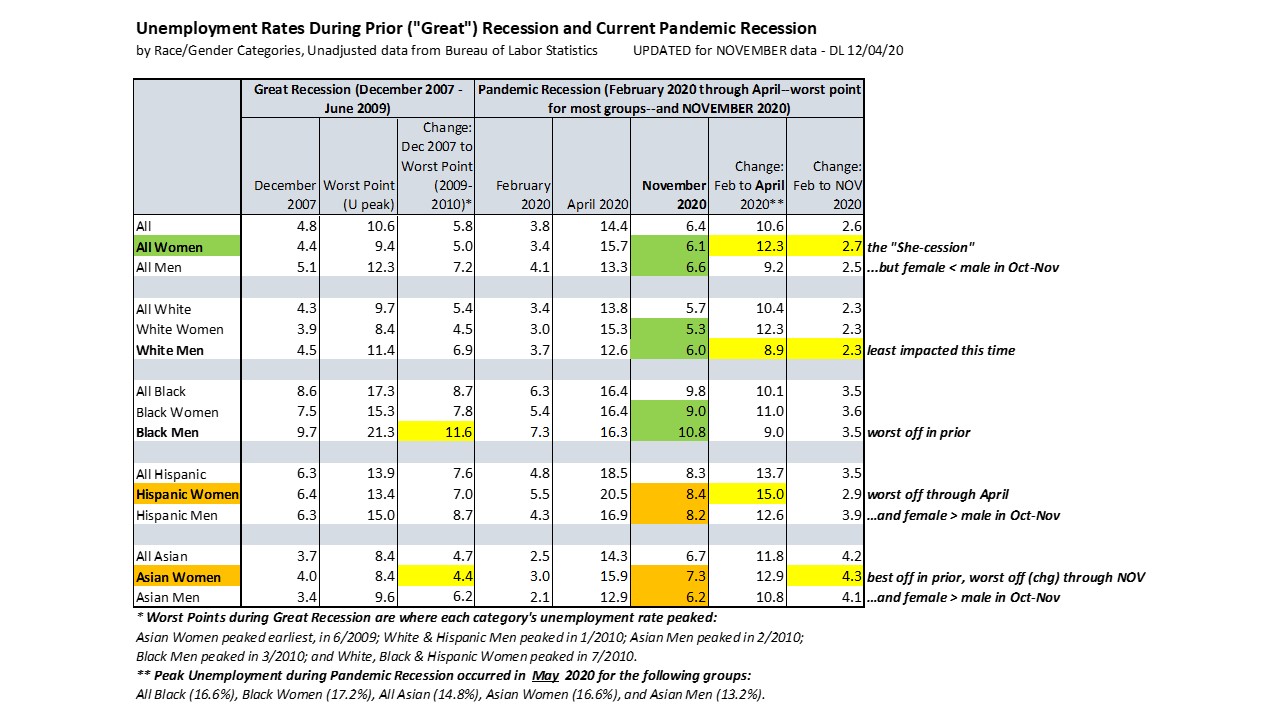

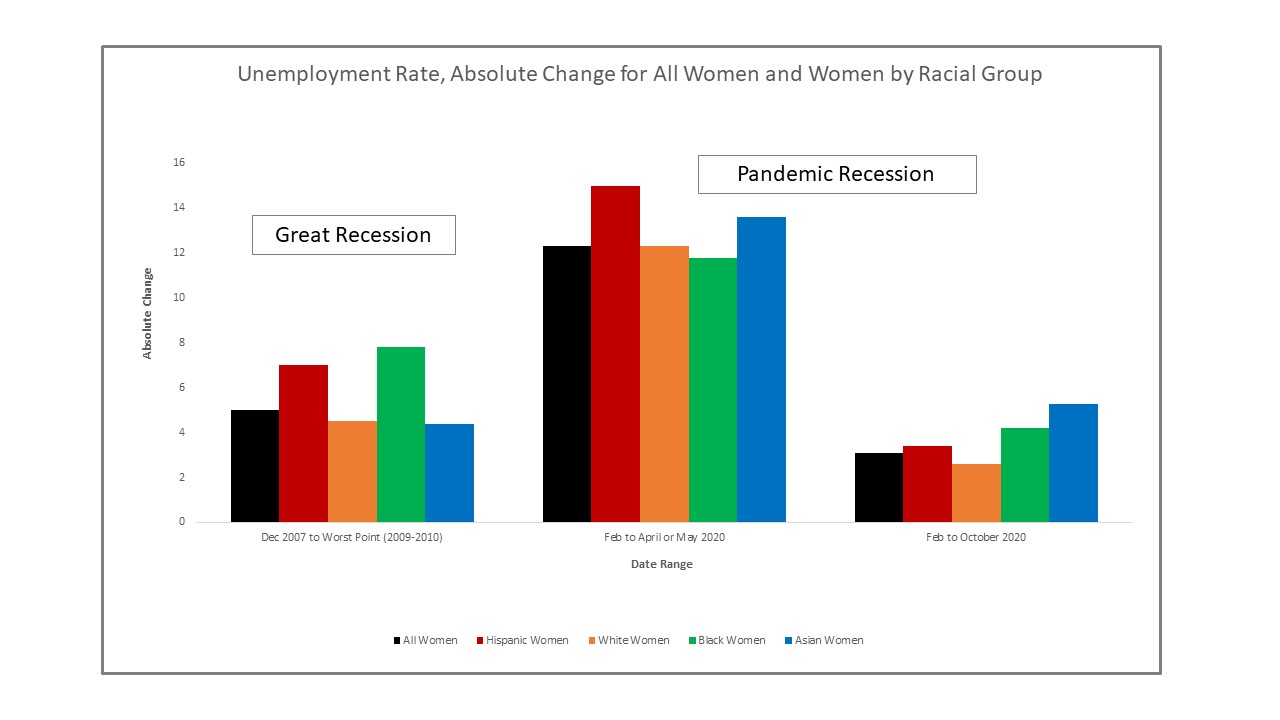

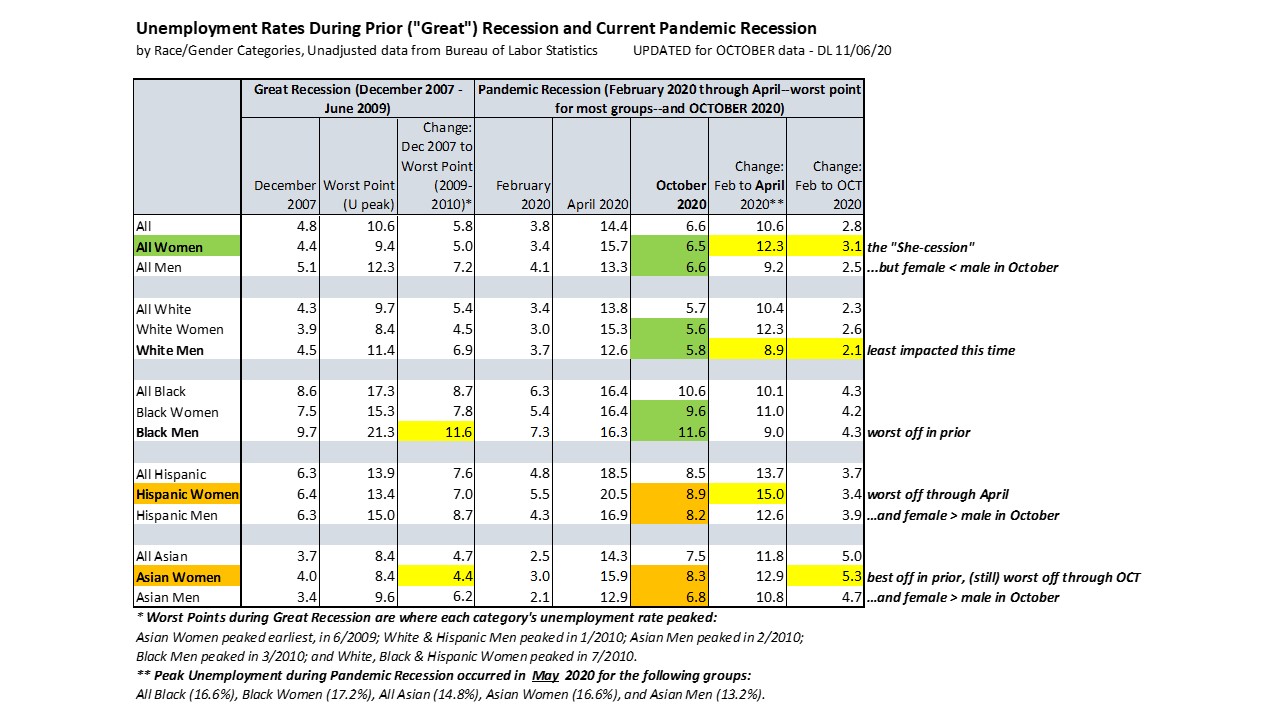

Absolute change in unemployment rates among women by race — comparing the Great Recession with the Pandemic Recession. The largest increases in unemployment have been among women of color–Hispanic and Asian women at the start of the Pandemic Recession, but through November (all groups of) women of color still had experienced larger increases in unemployment than White women.Unemployment rate for all in the labor force (age 16+), all men (blue), and all women (red), during the Pandemic Recession (Feb-Nov 2020). Note that female unemployment surged past men’s at the peak of the recession in April, but since October, the overall male unemployment rate has exceeded the female rate.Female unemployment rates by race since January 2019. Before the pandemic, Asian women (blue line) typically enjoyed the best labor market outcomes and experienced the lowest unemployment rates, but in this Pandemic Recession their unemployment has increased the most and they have looked much more like other women of color (Hispanic/Latina and Black women) than like White women. In November, Asian female unemployment was still two full percentage points above White female unemployment. Male (blue) and female (red) employment-to-population ratios during the Pandemic Recession (Feb 2020 – Nov 2020). Hard to see any interesting differences by gender when everyone is lumped together/averaged out! (Note that men have always had higher E/pop and the male and female levels appear to have moved together during this recession.)Differences by race (men and women combined) in employment-to-population ratios are clearer. Note that Hispanics started out with highest E/Pop and dropped the most in the spring but have also recovered the most since the spring.Looking at women by race, we see clear differences in the levels and trends of E/pop. Note that Asian women (in blue) for much of 2019 had the second-highest E/pop (closest to Black women, in green), but looked more like Hispanic women (in red) this recession and as of November had the lowest E/pop among all women by race.Summary table of unemployment rate levels and changes for all race-gender categories, comparing the Great Recession with the Pandemic Recession.

Top line story is that yes, this Pandemic Recession has been one that’s disproportionately burdened women and especially women of color, but as the months are approaching a year, we’re seeing that even White men will not come out unscathed. With today’s report on the November employment situation–the rise in long-term unemployed, the slowing of the recovery in labor force participation and the employment-to-population ratio as people sit themselves on the sidelines (hunker down at home) and literally “wait” for the public health crisis to end–we can see that the labor market impacts we’ve suffered so far are going to take awhile to recover from.

For students who are looking for a job in their specialty, an important factor is the presence of an essay, many resort to quality essay writing service. In the present conditions, the competition for a job is very high.

For economic policy to be most helpful to the labor market recovery, it will have to address all the conditions that are holding back work both at the workplace (the demand side, where certain places and types of work are still not safe to return to) and the home (the supply side, where many parents are now full-time caregivers given school closures). This is truly not a typical economic recession–it is not just dubbed the “Pandemic Recession” but is literally driven by the pandemic. So first and foremost, we need to get the public health crisis under control. (And that means listen to Dr. Fauci’s advice about wearing our masks and avoiding social gatherings as we wait for our vaccine.)

With Joe Biden having won the presidency as of yesterday (11/7/20), the new labor market data that came out the day before was amazingly aligned with voting patterns, which show men more often voting for Trump, women and especially women of color more often voting for Biden, and Trump (vs. Biden) voters more likely to put the economy (vs. the pandemic) as their biggest concern. The Bureau of Labor Statistics’ report on the monthly employment situation, and their underlying survey data (not all published in the report but accessible here and here) show that while the labor market continues to improve since its worst point this spring, the continued severity of the pandemic continues to weigh on women’s work far more than men’s. The “SheCession” (or is it “She-session” as Heather Long of the Washington Post recently called it… either works to me) is still an acute condition, particularly for women of color.

Below are the latest numbers (in table and charts) on unemployment by race and gender categories and comparing the current Pandemic Recession to the Great Recession. Through September, only Asian women were still at a higher level of unemployment than at the worst point of the Great Recession. As of the latest data for October, all race-gender categories have seen unemployment continue to fall to the point where even Asian women are now (slightly) better off (at 8.3% unemployment) than they were at the worst point of their Great Recession experience (which was 8.4%).

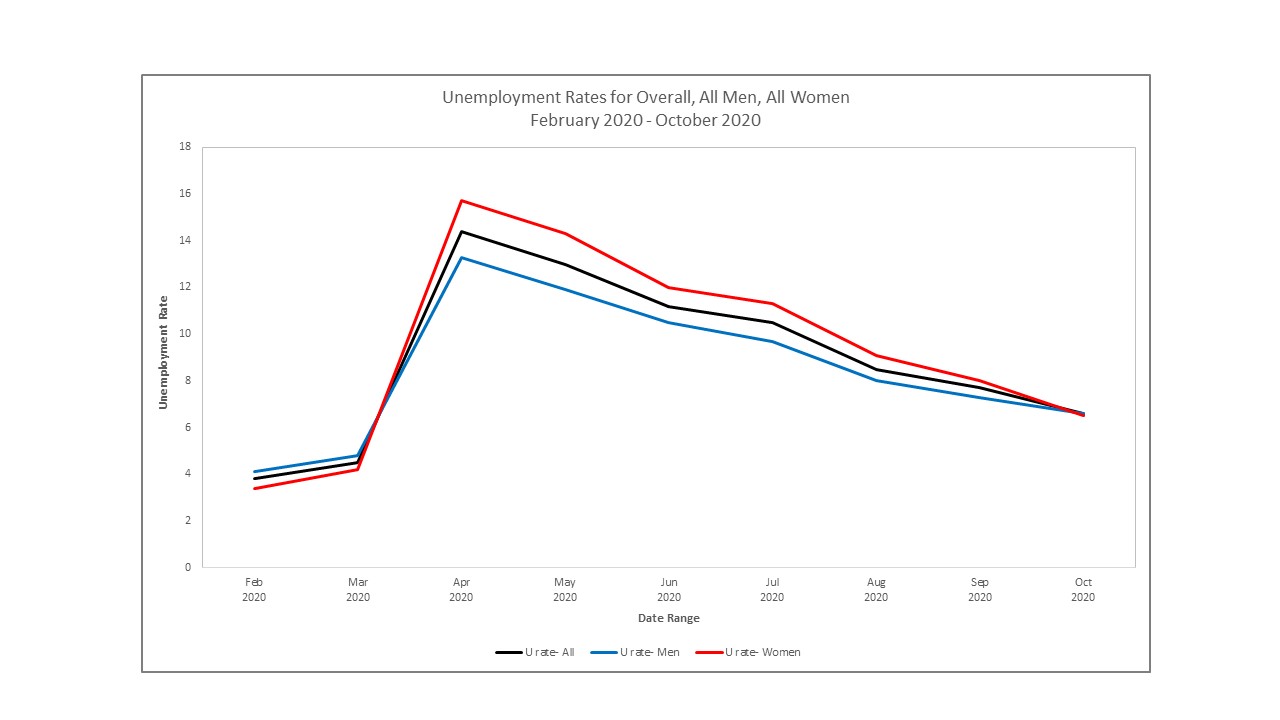

October is the first month since the start of the pandemic that we saw the overall female unemployment rate (at 6.5%) fall below the overall male unemployment rate (at 6.6%). But the differences across race are stark: among Hispanics and Asians, female unemployment still exceeds male unemployment. Factors driving the “SheCession” on both the demand and supply sides of the labor market make the explanations complicated and impossible to generalize. (Further interdisciplinary study–starting with interviews and focus groups, then moving to more detailed surveys and analysis of collected data–is needed.)

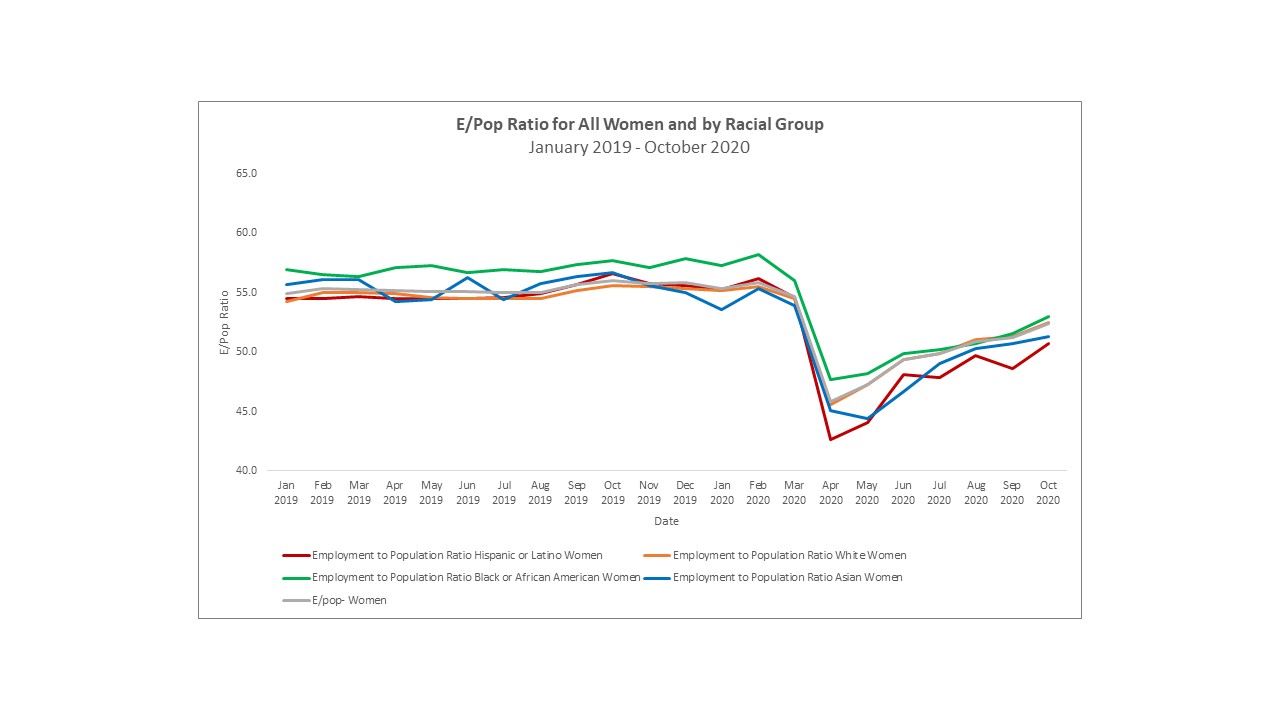

The larger toll of the pandemic on working women doesn’t just show up in the unemployment rate measure–which is still nearly double its February pre-pandemic rate and which can be misleadingly reduced when people drop out of the labor force entirely, which reduces the numerator (# of unemployed) by a larger proportion than the denominator (# in labor force = # unemployed + # employed). The “SheCession” also shows up in the employment-to-population (E/Pop) ratio:

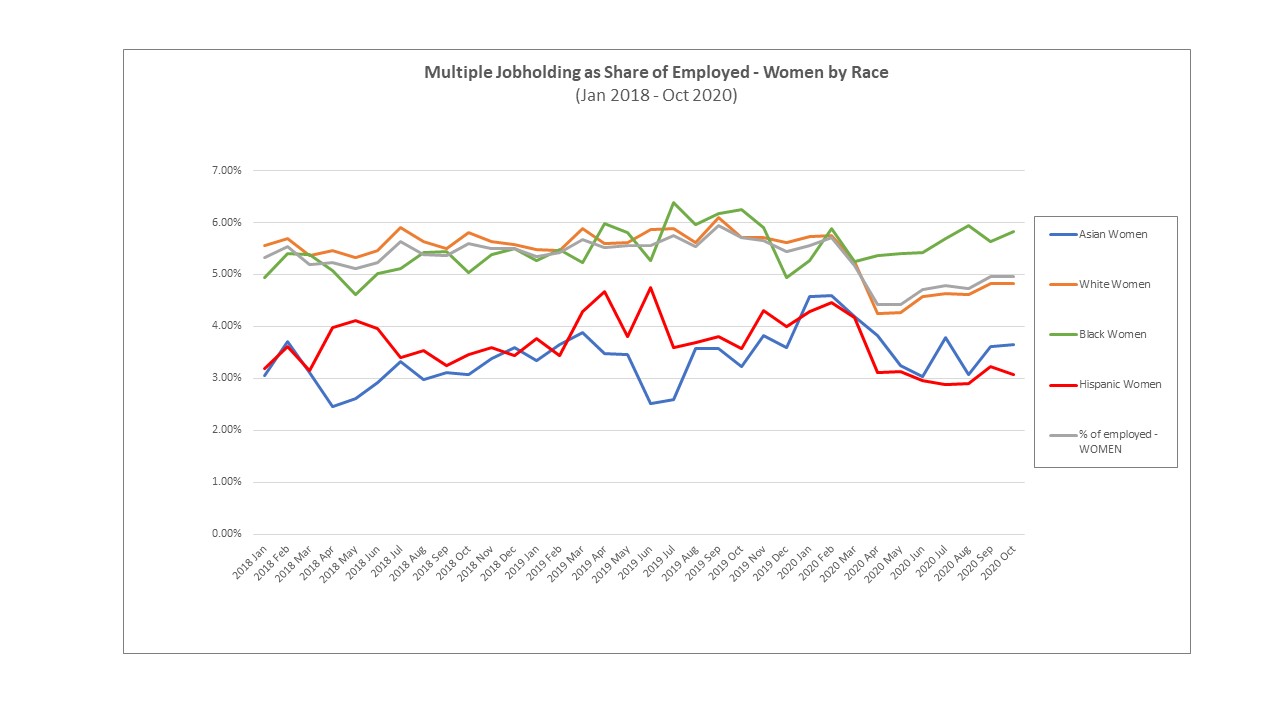

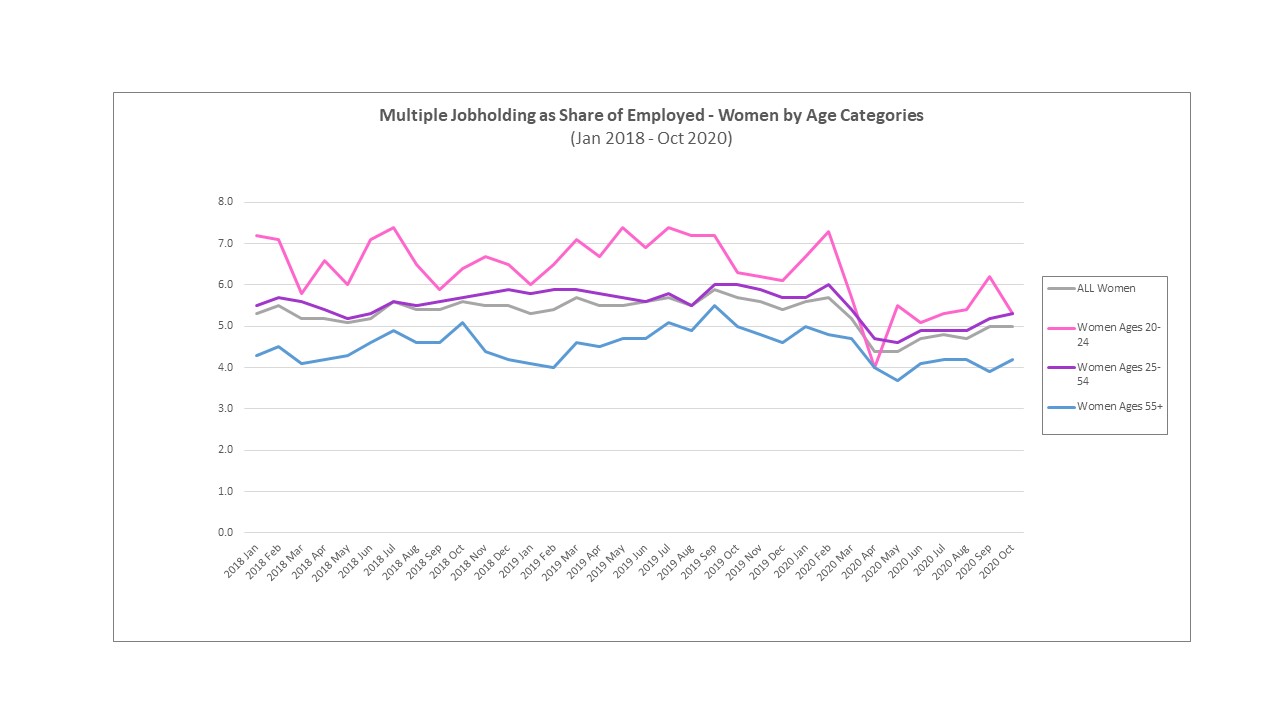

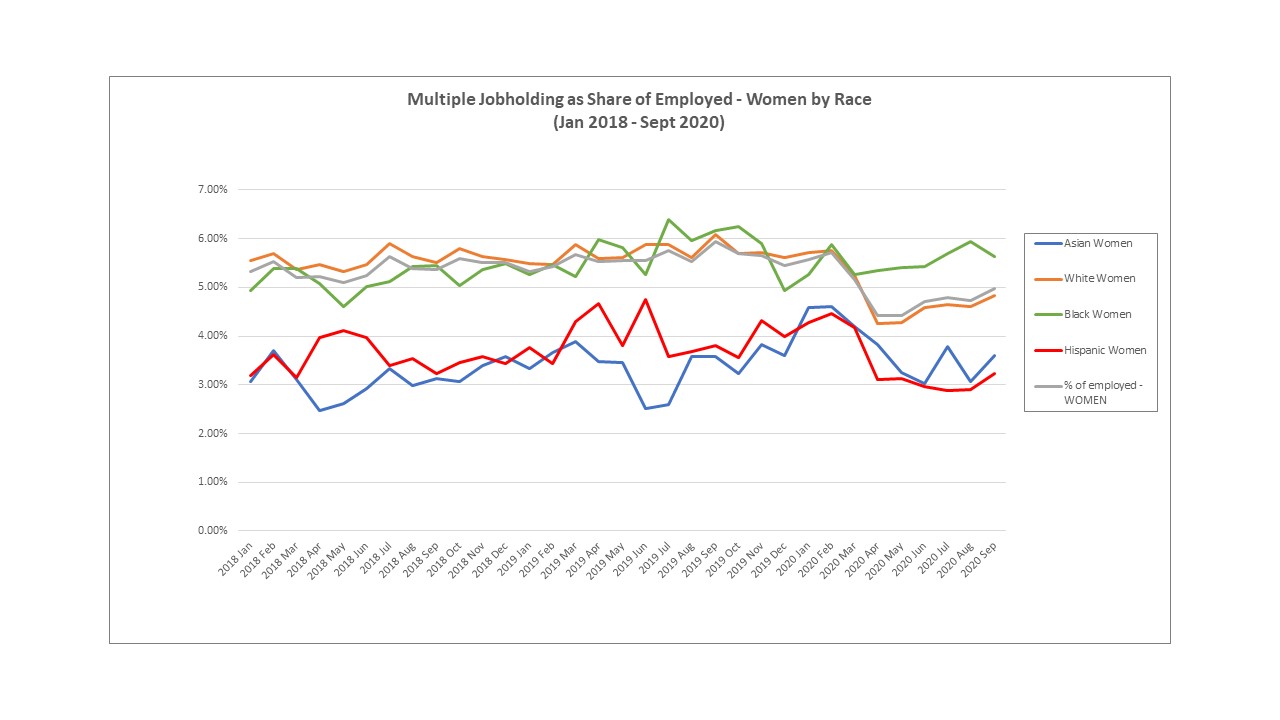

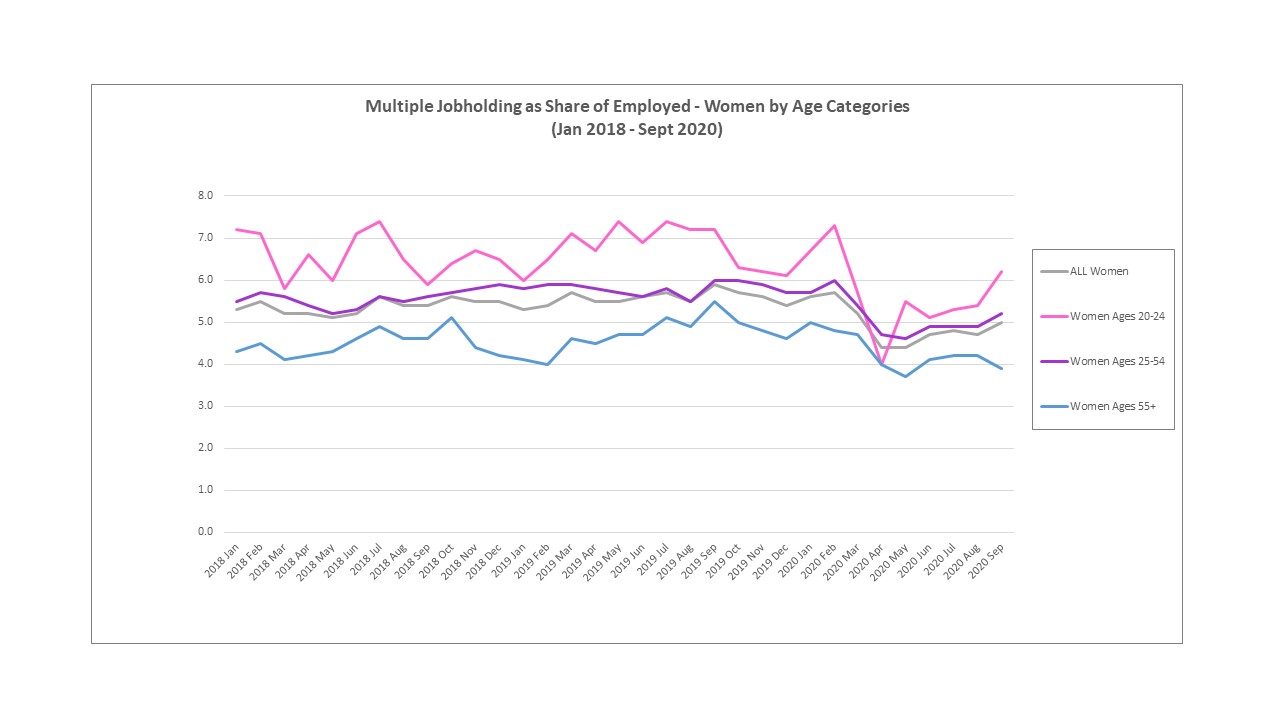

And the SheCession shows up in the multiple jobholding data, where working women more commonly than men work two or more jobs (as has always been true because women more commonly work part-time rather than full-time jobs whether by preference or not), but in the pandemic recession have had to piece together and juggle multiple jobs along with their unexpected and unpredictable caregiving responsibilities at home. Note that during the pandemic we have seen the distribution of multiple jobholding among women widen across both race and age categories–with Black women and the youngest women most likely to be working multiple jobs:

To follow up on last week’s post showing how women are still more likely to be working multiple jobs than men (both among the employed and among their total populations), here’s a reminder that not all women are the same. Let’s look at multiple jobholders as a share of employed, across race and age categories.

Black women are substantially more likely to hold multiple jobs than any other race categories of women. Notably, while multiple jobholding fell for all groups in the spring when unemployment peaked (and number of overall jobs in the economy cratered), multiple jobholding as share of employed has already (as of September) returned to a “normal” level for Black women but not for other women.By age categories, the youngest of working women (ages 20-24) have always been the most likely to hold multiple jobs, because they are most likely to have to piece together multiple part-time jobs (often in the leisure/hospitality sector) to make a living. These women were most likely to lose at least one of their multiple jobs at the start of the pandemic, and regain work as businesses reopened in the summer.

There are many factors that could explain the differences by race, probably most significantly that Black women are more likely to be sole earners in their households (as well as single parents) yet also more likely to earn lower hourly wages. The different trends by age reflect that multiple part-time jobs are often the closest a young adult (even a college-educated one) can come to a full-time job–and that the human-service-intensive jobs many young women work in were the ones that disappeared the most at the start of the pandemic and have not and will not likely fully come back even when the public health crisis eventually wanes. The Pandemic Recession — or “She-cession”– has not just been hard on women because of the severity of the lowest depths of job loss experienced, but because it’s really “jerked around” the women who were already the most economically vulnerable.

Last summer –as in all the way back in 2019–I wrote this post about how multiple jobholding had become more common in the labor force overall and how this seemed to be a “new normal” for the (very strong 2019) economy–something no longer limited to recessionary times when people might be forced to piece together several smaller jobs when they couldn’t get a full-time job. I underscored my finding that multiple jobholding was becoming especially more prevalent among working women, and I hypothesized on some reasons why, including: (i) women need multiple jobs to add up to the pay of one job (because women typically earn less than men); (ii) women choose to work multiple jobs to add up to the hours of one full-time job–yet with the greater flexibility/control over work schedule that multiple part-time jobs allow; and (iii) women often choose to “work” not to maximize earnings but for personal fulfillment, which often calls for a variety of work whether paid or underpaid or unpaid, rather than just one job.

In 2019 all these reasons were already, in the slow-but-steady recovery from the Great Recession, becoming part of the “new normal” of an economy and labor market increasingly dominated by women. Last week I learned of this new Census analysis based on a new measure of multiple jobholding:

We create a measure of multiple jobholding from the U.S. Census Bureau’s Longitudinal Employer-Household Dynamics data. This new series shows that 7.8 percent of persons in the U.S. are multiple jobholders, this percentage is pro-cyclical, and has been trending upward during the past twenty years. The data also show that earnings from secondary jobs are, on average, 27.8 percent of a multiple jobholder’s total quarterly earnings. Multiple jobholding occurs at all levels of earnings, with both higher- and lower-earnings multiple jobholders earning more than 25 percent of their total earnings from multiple jobs. These new statistics tell us that multiple jobholding is more important in the U.S. economy than we knew.

“A New Measure of Multiple Jobholding in the U.S. Economy,” by Keith A. Bailey and James R. Spletzer, Working Paper #CES-20-26, September 2020.

So the Census researchers conclude that multiple jobholding is pro-cyclical (no longer just a “make ends meet in hard economic times” phenomenon), has been rising in prevalence over the past 20 years (not even just since the Great Recession), and “is more important in the U.S. economy than we knew.” They might as well have said that the role of women in the workforce, and how women choose to work, is more important than we knew.

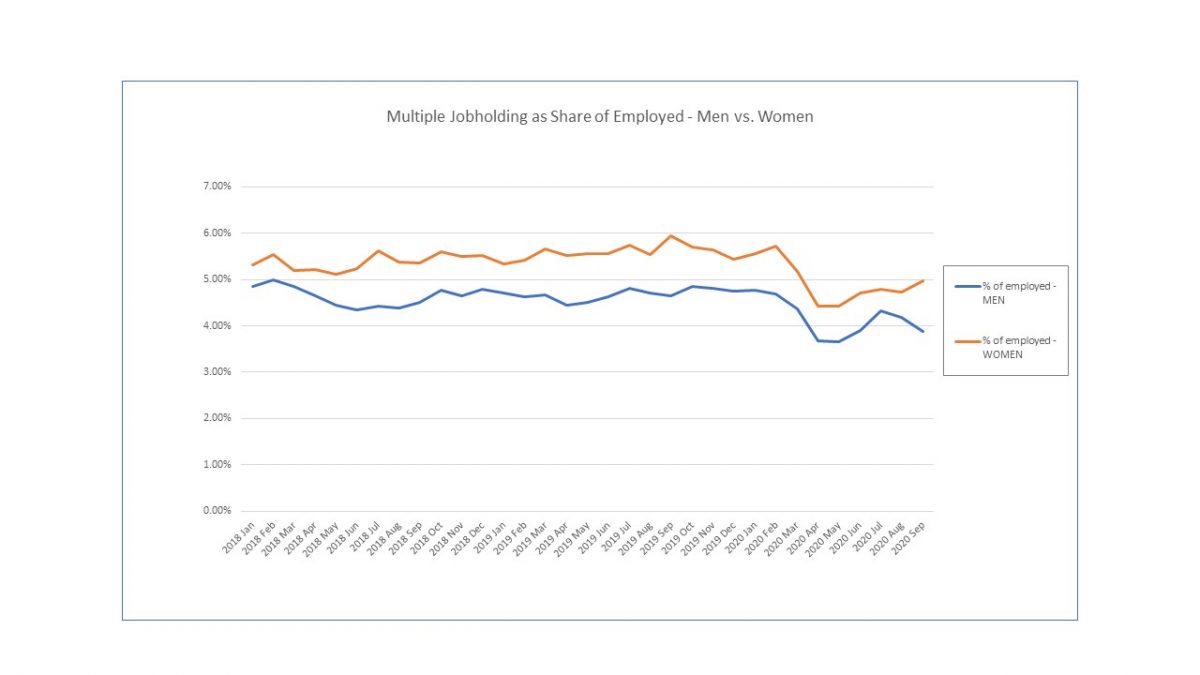

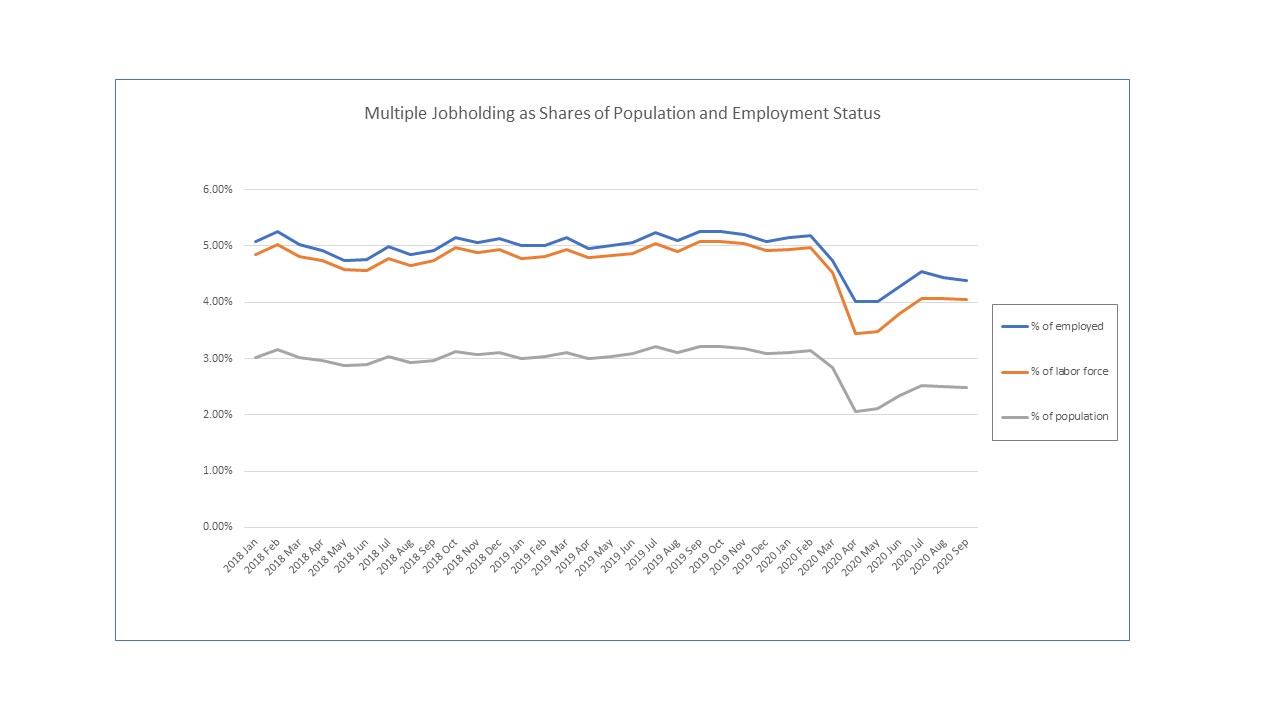

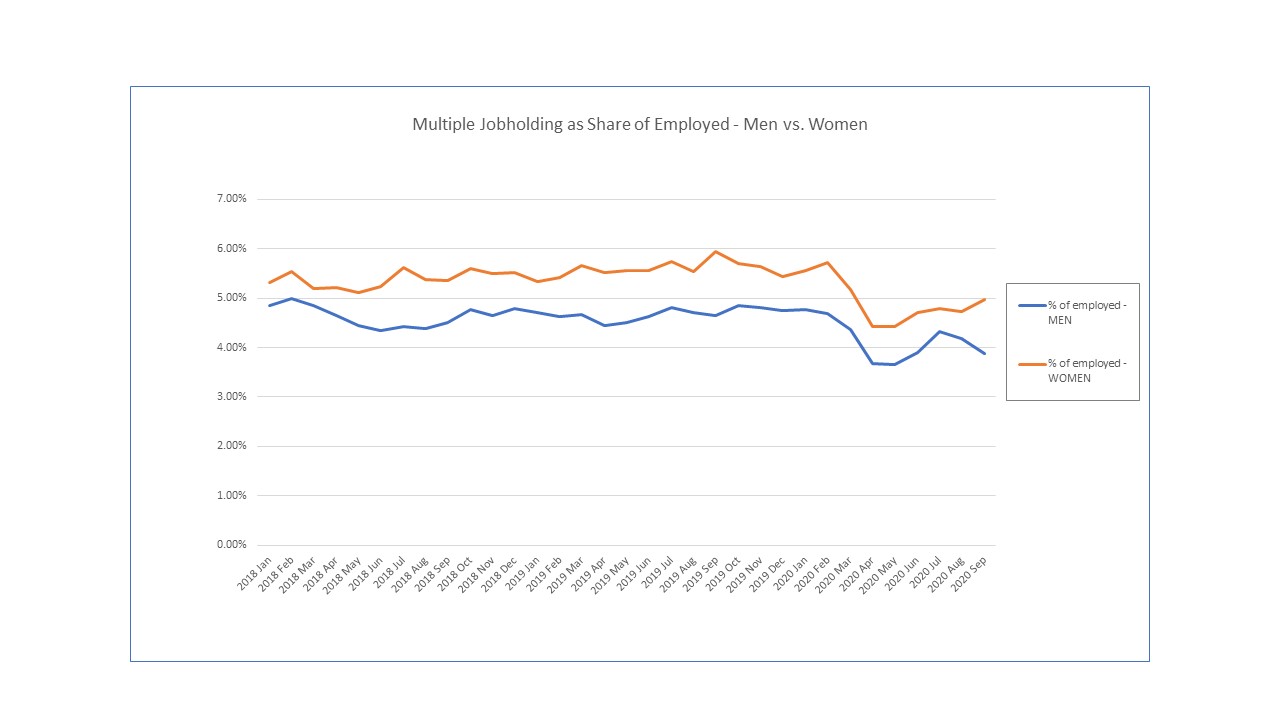

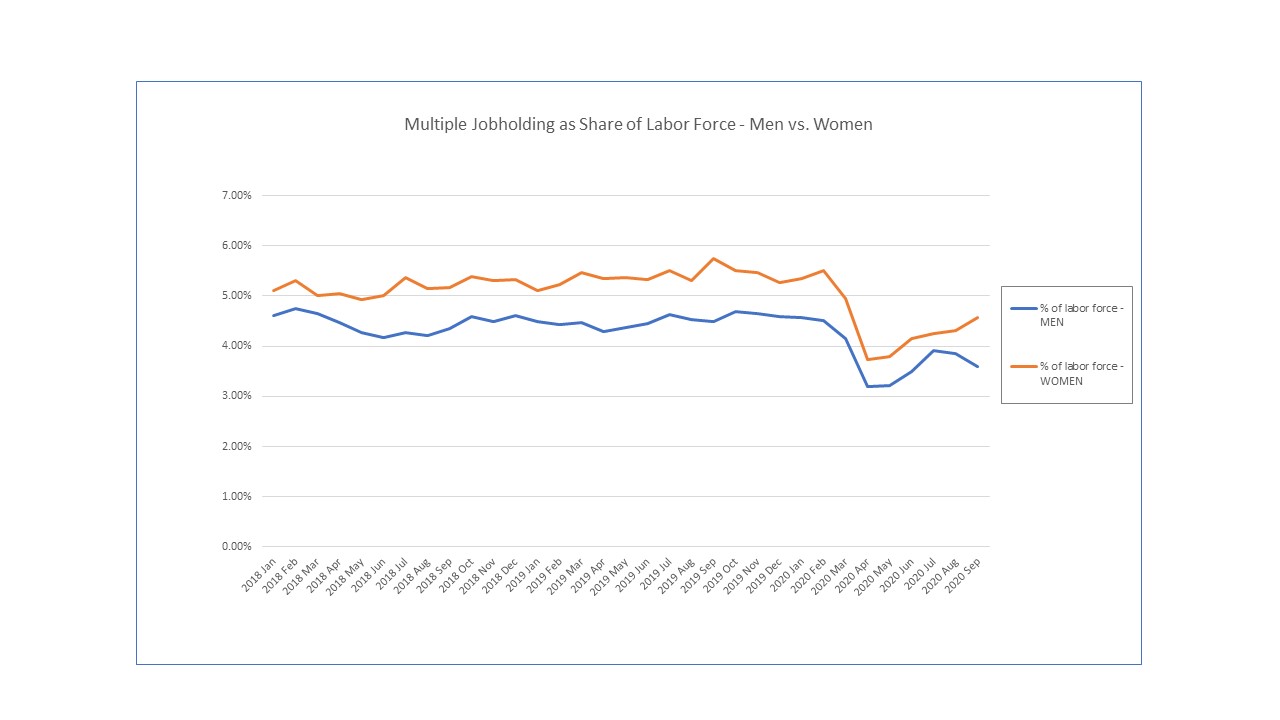

This prompted me to go back to my summer 2019 blog post and update the data through September 2020 (the latest monthly employment statistics from household survey data) to see what the past year looks like in terms of multiple jobholding and its prevalence among workers overall and men vs. women. Here are some charts that look at multiple jobholding as share of people who are employed, in the workforce (“labor force” meaning employed or unemployed/looking for work), and relative to total population–and then comparing each of the three shares for men vs. women. All charts show BLS unadjusted monthly household employment survey data for populations age 16+, from January 2018 through September 2020:

Shares of total (men+women) population measures: Overall, multiple jobholding dropped dramatically from February to April 2020 at the start of the Pandemic Recession as the number of jobs in the overall economy plummeted, and as of September is still below what had been the “new normal.”As share of total employed, comparing men (blue) vs. women (orange). Note that multiple jobholding in the recovery (thus far) from the Pandemic Recession first rose for both men and women, but since July has decreased among working men while increasing among working women.As share of those in the labor force, we see basically the same story as among those employed; since July, women’s multiple jobholding has increased while men’s has decreased.And even as a share of their total population, women are more likely to be multiple jobholders than are men.

In summary, we see that multiple jobholding has come down and then back up during the pandemic, along with jobs and employment in general. Women still juggle a lot of jobs, whether paid work in the labor market or unpaid work at home. Even as workers have lost some of their multiple jobs and have yet to fully regain them, we see that multiple jobholding is a significant phenomenon in the U.S. economy and one that is not necessarily a bad thing if it has made it easier for workers–especially working women–to better tailor their work opportunities to their personal circumstances and preferences. Women have always chosen multiple part-time jobs so that work fits into the rest of their lives better, even pre-pandemic. With the pandemic placing only more burdens and constraints on women’s time (with kids and elderly parents to care for), multiple jobholding will become an even more important way for women to stay connected to the workforce. But multiple part-time jobs have never added up to the level of economic reward one can get from one full-time job–whether it be in the form of wages or benefits (such as subsidized health insurance, childcare assistance, and paid leave). Women are too easily relegated to “secondary earner” status (read: “you should be the one to stay at home now”) which makes it too common for them to disengage from market work when family circumstances change. The way women juggle their different jobs at home and at work will require a lot more attention and focus from economic policymakers if we want our economy to not just “survive” this pandemic recession but to actually “thrive” over the longer term.